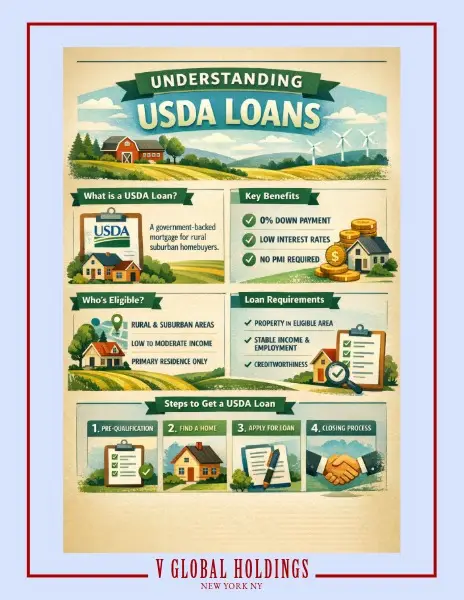

USDA loans are special mortgage options designed to help low- and moderate-income homebuyers, particularly in rural areas. These loans require no down payment and are backed by the U.S. Department of Agriculture, making homeownership more accessible for those who qualify. This financial support encourages growth in rural communities by providing individuals and families the opportunity to purchase homes.

Eligibility for USDA loans depends on several factors including income and the location of the property. Many potential homeowners may be surprised to find that they can qualify for advantageous financing, even without substantial savings. Understanding these loans can open new doors and opportunities for many individuals seeking to buy a home in less populated areas.

Understanding USDA Loans

USDA loans help people achieve homeownership in rural areas. They are designed to make it easier for low- to moderate-income buyers to secure financing without large down payments.

Definition and Purpose of USDA Loans

USDA loans are mortgage options backed by the U.S. Department of Agriculture. Their main goal is to promote homeownership in rural communities. These loans help people who may not qualify for traditional financing due to income limits or lack of savings.

USDA loans typically do not require a down payment. This makes them appealing to homebuyers who have limited savings. They also offer competitive interest rates, which can lower monthly payments. Additionally, they support rural development, boosting local economies.

Types of USDA Loans

There are two main types of USDA loans: Guaranteed loans and Direct loans.

Guaranteed loans are issued by approved lenders, like banks and credit unions. The USDA guarantees a portion of the loan, making it less risky for lenders. This type is available to moderate-income families who meet specific eligibility requirements.

Direct loans are offered directly by the USDA to low-income applicants. These loans have more flexible income limits and often come with lower interest rates. Direct loans aim to assist buyers who may not qualify for conventional loans due to financial constraints.

Both types aim to enhance homeownership and foster rural community development.

Eligibility Requirements for USDA Loans

USDA loans are designed to help low- to moderate-income families buy homes in eligible rural areas. Several factors determine eligibility, including property location, household income limits, and other qualifying criteria.

Property Eligibility

To qualify for a USDA loan, the property must be located in an eligible rural area. The USDA maintains a Property Eligibility Program that provides a searchable database for potential buyers. Properties typically include single-family homes, but they cannot be in urban areas.

Eligible properties must meet specific conditions, such as being modest in size, design, and cost. Buyers should check the USDA’s website to find if a specific address qualifies. If the property is not eligible, buyers cannot receive the loan.

Household Income Limits

USDA loans have income limits based on the household size and area median income. For a household to qualify, the total income should generally not exceed 115% of the area’s median income. Income limits vary by location, so it is crucial for applicants to verify the limits for their county.

The USDA also considers all sources of income, including salaries, bonuses, and social security. Applicants can use the USDA income and property eligibility site to calculate their income. This information is vital when applying for a USDA loan.

Other Qualifying Criteria

In addition to property and income limits, several other criteria exist. Applicants usually need a credit score of at least 620. They must also demonstrate a stable income and manageable debt-to-income (DTI) ratio, typically below 50%.

USDA loans require a guarantee fee of 1% upfront and an annual fee of 0.35% of the loan amount. Potential borrowers must also show they can manage typical homeownership costs. All these factors contribute to a final determination of loan eligibility.

Application Process for USDA Loans

The application process for USDA loans involves several key steps. Understanding how to prepare your application and what to expect during the submission and review phases can help streamline the experience.

Preparing Your Application

To start, applicants must gather essential documents. This includes proof of income, credit history, and information about assets and debts. Accurate and complete information is crucial. Missing details can delay the process or lead to rejection.

Using the USDA website, individuals can access resources like the Loan Assistance Tool. This tool guides applicants step-by-step through the necessary forms. Applicants should also consider working with an approved lender. The lender will assist in ensuring that the application meets all requirements.

Submission and Review

Once the application is complete, it must be submitted to an approved lender. The lender will then review the application for accuracy and compliance. They work closely with USDA’s Rural Development staff during this phase.

Typically, the review process includes verifying all submitted information. This step ensures eligibility for either a direct loan or a guaranteed loan. If everything checks out, the lender will submit the application to USDA for final approval. It is important to stay in communication with the lender throughout this period to address any questions or additional requirements promptly.

Benefits and Limitations of USDA Loans

USDA loans offer unique advantages for homebuyers in eligible rural areas, especially regarding financing options. However, there are also important limitations to consider when applying for these loans.

Advantages of Using a USDA Loan

One of the primary benefits of a USDA loan is the zero down payment requirement. This feature makes homeownership accessible for individuals who may struggle to save for a traditional down payment.

Additionally, USDA loans typically come with lower interest rates compared to conventional loans. This can result in lower monthly payments, making it easier to manage finances.

The loans are designed to promote development in rural areas, encouraging homeownership among people who might not otherwise qualify for financing. Furthermore, these loans have flexible credit requirements, which can benefit first-time buyers or those with less-than-perfect credit histories.

Potential Drawbacks

While USDA loans have many advantages, they also come with some limitations. One major factor is that these loans are only available for homes located in eligible rural areas. This may limit options for buyers who want to live in more urban settings.

Additionally, there are income limits associated with USDA loans. If a borrower’s income exceeds a certain threshold, they may not qualify for the program.

Another consideration is that USDA loans involve specific fees, including an upfront guarantee fee and an annual fee. These costs can add to the overall expense of the loan. Buyers should weigh these factors against the benefits to determine if a USDA loan is the right fit for their situation.

Supporting Rural America

USDA programs play a vital role in enhancing the quality of life in rural areas. They offer financial support for agricultural needs while promoting community development. This commitment contributes to the growth and sustainability of rural America.

USDA’s Impact on Rural Development

USDA Rural Development focuses on improving rural living conditions. It provides funding for infrastructure, such as roads and water systems, which are essential for community growth. Significant investments, like the announced $1.1 billion for infrastructure upgrades, help create jobs and ensure access to clean water and reliable electricity.

USDA programs also invest in modernizing electric infrastructure, benefiting millions. By offering loans and grants, USDA supports local governments and organizations in building necessary facilities.

Financial Assistance for Agriculture

Farmers and ranchers can access several financial options through the USDA. The Farm Service Agency (FSA) offers loans for purchasing land, livestock, and equipment. These loans can also be used for farm improvements and buying supplies.

Additionally, assistance includes grants that help farmers implement renewable energy projects. This funding not only boosts productivity but also encourages sustainable practices. This dual support allows agricultural businesses to grow and thrive in a competitive environment.

Rural Business and Community Programs

USDA empowers rural businesses through targeted programs. It operates financial assistance programs tailored to various rural needs. Small business loans and grants help entrepreneurs start or expand operations.

Community programs also focus on enhancing local services. Initiatives aimed at improving education, health, and safety strengthen the fabric of rural life. By funding projects that align with community needs, USDA fosters economic growth and improves residents’ quality of life.

In summary, through various funding and support mechanisms, USDA plays a crucial role in supporting rural America.

Homeownership Resources

There are various resources available to support individuals and families interested in homeownership. These resources include educational materials and counseling to help navigate the process, as well as additional USDA assistance programs beyond loans.

Educational Materials and Counseling

USDA provides a wealth of educational materials to help potential homeowners. Their resources guide individuals through budgeting, home maintenance, and the loan application process.

Counseling programs are available through local organizations. These sessions cover topics such as credit management and the benefits of homeownership. For example, the Martin family, who utilized these resources, found valuable guidance that helped them secure their home.

Homeownership Month promotes awareness and encourages informed decisions in this area. Workshops are often held during this time, offering essential tools to first-time buyers.

USDA Assistance Beyond Loans

USDA offers programs beyond just loans, which can greatly benefit families. For instance, the Single Family Housing Repair Loans and Grants program assists low-income homeowners in making repairs. This helps maintain safe and decent living conditions.

Additionally, multi-family housing programs are available for those seeking rental assistance in eligible areas. These programs aim to provide stable housing options, particularly in places like the St. Regis Mohawk Reservation.

To further enhance their effectiveness, USDA emphasizes risk management. They offer tools to help families evaluate their financial situations and make informed choices regarding homeownership and maintenance.

Frequently Asked Questions

USDA loans are designed to help people purchase homes in rural areas. They come with specific requirements, benefits, and differences compared to other loan types. Below are common questions related to USDA loans.

What are the requirements for obtaining a USDA loan?

To qualify for a USDA loan, the applicant generally needs to meet certain income limits. These limits vary based on the area and family size. Additionally, the property must be located in a designated rural area.

How do USDA Rural Development loans work?

USDA loans provide financial assistance to eligible applicants aimed at promoting homeownership in rural regions. These loans often require no down payment and provide competitive interest rates. The payment assistance reduces monthly mortgage costs for qualifying borrowers.

What are the differences between USDA loans and FHA loans?

USDA loans are specifically for rural properties, whereas FHA loans can be used for homes in urban or suburban areas. USDA loans typically offer no down payment, while FHA loans usually require a down payment of at least 3.5%. The eligibility criteria and insurance costs also differ between the two.

Are there specific eligibility criteria for USDA loans?

Yes, USDA loans have specific eligibility criteria. Income must be at or below 115% of the area’s median income. The applicant must also have good credit and demonstrate reliable repayment ability. The property must meet USDA location and condition standards.

What are the benefits of securing a USDA loan for housing?

USDA loans offer several advantages. They usually require no down payment, making homeownership more accessible. The loan terms often feature lower interest rates compared to conventional loans. Additionally, there is no need for private mortgage insurance (PMI), which lowers monthly costs.

Is it difficult to qualify for a USDA loan?

Qualifying for a USDA loan can be straightforward if the applicant meets the income and credit requirements. It is typically less difficult than qualifying for a conventional loan that may have stricter down payment and credit score criteria. Consulting with a lender can help clarify eligibility.