What is Private Credit?

Private credit is debt financing provided by non-bank lenders to companies through privately negotiated, non-traded loans, representing a fundamental shift in corporate financing away from traditional banking systems[8][6]. The market has experienced exponential growth since the 2008 financial crisis, expanding tenfold to reach approximately \$2-3 trillion in assets under management as of early 2026[8][9].

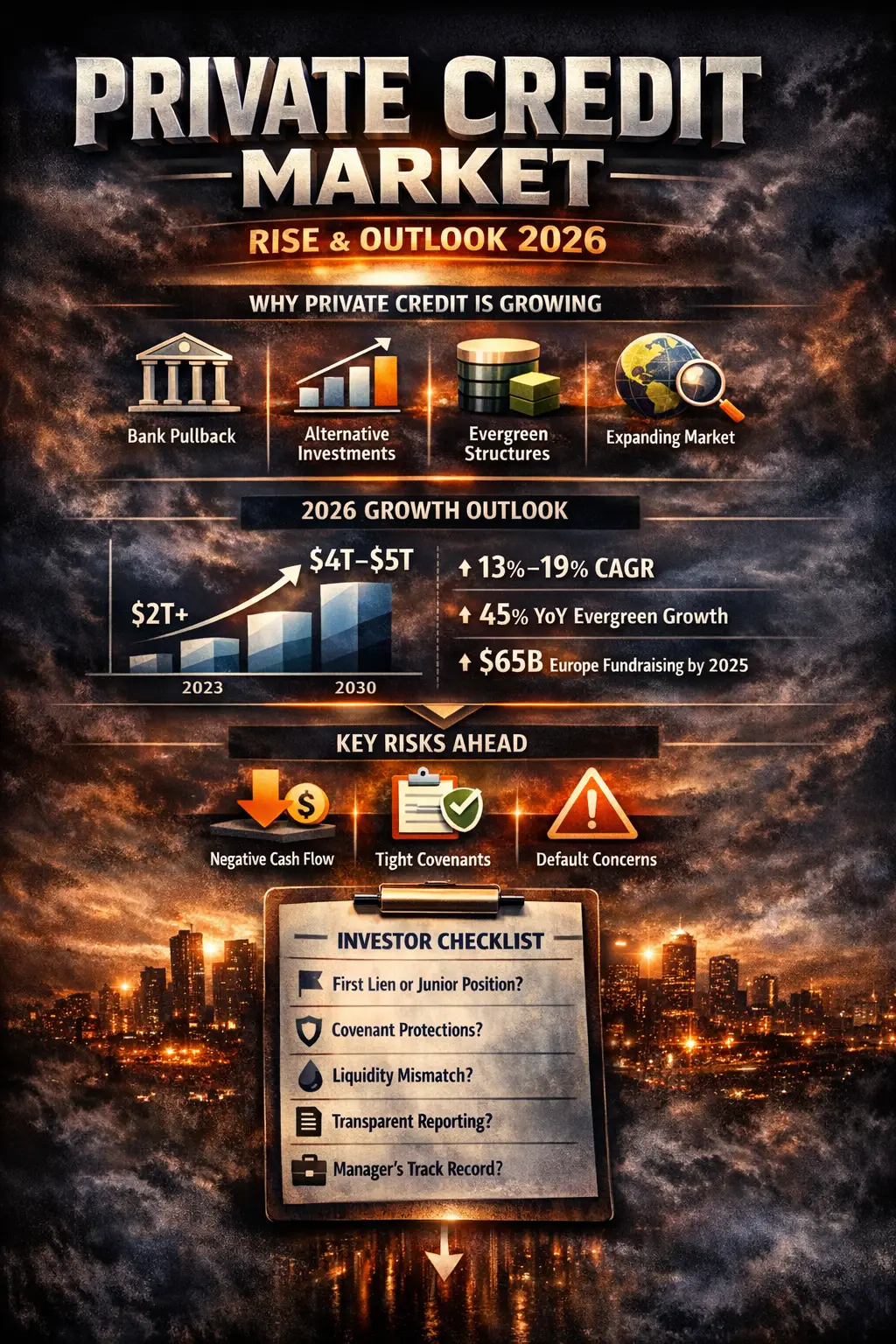

2026 growth projections indicate continued robust expansion, with market size expected to exceed \$2 trillion (conservative estimate) to \$3.4 trillion (aggressive estimate), representing implied growth rates of 13.6-18.9% annually through 2030[1][13]. Growth is driven by bank lending retrenchment (particularly Basel IV implementation in Europe), institutional capital migration to alternative assets, perpetual capital structure innovations (evergreen funds growing at 45% year-over-year), and expanding addressable markets exceeding \$30 trillion[2][1].

The asset class distinguishes itself through floating-rate structures, senior-secured positions, customized loan terms, and illiquidity premiums yielding 200-250 basis points above public leveraged loans[1]. However, the market is transitioning from yield-driven momentum to discipline-focused underwriting as regulators increase oversight and credit quality concerns emerge[13][17].

1. What is Private Credit — Core Definition and Market Structure

Definition and Distinguishing Characteristics

Private credit refers to debt financing provided by non-bank lenders to private and public companies through privately negotiated loans that are not traded on public markets[8]. Also known as private debt, it represents lending and borrowing outside the traditional banking system, filling the void created when banks pulled back from business lending following the 2008-2009 Global Financial Crisis[8][6].

These are bilateral loan agreements between individual borrowers and non-bank lenders, often referred to as “direct lending,” though deals involving a small group of lenders (“club deals”) also fall under this category[8]. Non-bank lenders providing private credit include private equity shops, alternative asset managers, private credit funds, and business development companies (BDCs)[8].

Key Structural Differences from Public Credit Markets

Private credit differs significantly from traditional banking and public credit markets across multiple dimensions[7][12]:

| Dimension | Private Credit | Public Credit/Traditional Banking |

|---|---|---|

| Market Structure | Privately originated and held, not traded | Publicly syndicated and actively traded |

| Customization | Highly flexible, tailored to borrower needs | Standardized terms |

| Interest Rate Structure | Nearly all floating-rate (SOFR/Treasury + spread) | Often fixed-rate |

| Credit Ratings | Not rated | Typically rated by agencies |

| Liquidity | Illiquid (5-10 year lock-ups) | Liquid, traded on secondary markets |

| Valuation Frequency | Infrequent (quarterly or less) | Continuous mark-to-market |

| Disclosure Requirements | Minimal (private transactions) | Extensive public disclosure |

| Yield Premium | 200-250 bps above leveraged loans | Market-determined spreads |

The customization premium is central to private credit’s value proposition—investors receive higher yields because loans are not actively traded and involve more customized structures than public fixed income[11]. Unlike publicly syndicated loans where banks sell loans to a broad group of lenders who trade these securities on public markets, private credit is privately originated and held, not traded[7][12].

Current Market Scale

As of late 2024, the private credit market surpassed \$3 trillion in total assets under management[8]. The Federal Reserve’s data shows that total private credit reached nearly \$1.7 trillion as of June 2023, with direct lending alone representing approximately \$800 billion (about one half of the total)[9]. This represents a tenfold increase from 2009 levels following the Global Financial Crisis[8].

Private credit has grown from representing approximately 5 percent of the US below-investment-grade credit market in the mid-2000s to more than 25 percent today[10], demonstrating its transformation from a niche financing source to a mainstream alternative to traditional banking.

2. How Private Credit Works — Transaction Mechanics and Fund Structures

Capital Sourcing and Fund Architecture

Private credit managers typically raise capital from limited partners (LPs) through specialized investment funds[8]. Increasingly, some of the largest private lenders maintain pools of perpetual or “evergreen” capital instead of raising discrete, closed-end funds, sometimes sourced from insurance providers or other institutions with long-term capital needs[8].

As of June 30, 2025, assets in evergreen private credit funds had reached \$644 billion, up 28% from the end of 2024 and approximately 45% year-over-year[2]—representing a structural shift toward permanent capital structures that provide greater deployment flexibility and reduced pressure from redemption cycles.

Loan Negotiation and Key Structuring Terms

The core advantage of private credit is flexibility in loan structure[8]. Key negotiable terms include:

Loan Size and Maturity: Average loan size has increased substantially, exceeding \$80 million since 2022—much larger than typical bank-dependent borrower loans[9]. Average maturity is approximately 5 years, with debt maturities spread evenly over coming years[9].

Interest Rate Structure: Private credit loans typically feature floating-rate structures rather than fixed rates[8][12]. Nearly all private credit loans are floating rate[9], with rates benchmarked to indices like SOFR (Secured Overnight Financing Rate) or Treasury yields[8]. A credit spread (measured in basis points) is added above the benchmark to compensate the lender for risk[8].

Collateral and Security: Most private loans are secured, with common collateral including accounts receivable, cash flow, inventory, equipment, and real estate[8]. An increasing share of private credit loans carry first liens on borrower assets[9], providing senior-secured status in default scenarios.

Covenants: Loan agreements include financial and operational conditions (covenants) that borrowers must maintain, such as minimum revenue thresholds or restrictions on additional debt[8]. These can range from covenant-heavy (for riskier borrowers) to covenant-lite structures[8]. Recent deals increasingly lack financial maintenance covenants[9], reflecting competitive dynamics.

Due Diligence and Ongoing Monitoring

Private lenders perform comprehensive due diligence on potential borrowers, focusing on creditworthiness and downside risk assessment[8]. The primary concern differs from PE/VC investing: lenders focus more on potential defaults than financial upside, since debt returns are capped at interest payments[8].

Once funded, lenders require regular financial statements from borrowers and monitor covenant compliance[8]. Unlike PE/VC investments with predetermined exit strategies, private credit has a predetermined timeline through its repayment schedule—assuming the borrower remains in good standing, the relationship ends once the loan matures[8].

3. Types of Private Credit Investments — Strategy Spectrum

Private credit encompasses multiple investment strategies, each with distinct risk-return profiles[12]:

Direct Lending and Senior Secured Loans

Senior-secured loans provided directly to middle-market companies represent the largest segment of private credit, comprising more than two-thirds of the market[9]. These loans typically occupy the top of the capital structure, offering the highest protections for investors[8][9] and the lowest risk, while generating steady current income[7][12].

A majority of these loans are backed by private equity sponsors[9], with top deal uses including general corporate purposes (working capital needs), debt refinancing, and private equity deals (leveraged buyouts and growth equity investments)[9].

Mezzanine and Subordinated Debt

Mezzanine debt is a hybrid instrument sitting between senior debt and equity in the capital structure[8][12]. It offers higher returns than senior debt to compensate for increased risk and frequently includes equity “kickers” in the form of warrants or conversion features[8][12]. About 15 percent of private credit takes the form of hybrid loan pari passu structures[9].

Distressed Debt and Special Situations

Distressed debt involves investing in the debt of companies in or near bankruptcy, with the goal of profiting from recovery or restructuring[8][12]. Special situations encompass non-traditional corporate events requiring high customization and complexity, such as M&A transactions, divestitures, or spinoffs[12].

Asset-Based Finance and Specialty Finance

Asset-based lending involves making loans secured by specific assets on a company’s balance sheet—such as accounts receivable, inventory, equipment, real estate, or infrastructure—with loan amounts tied directly to collateral value[8][12]. This includes real estate projects requiring significant upfront capital before generating revenue[8].

Specialty finance strategies include lending in niche areas like equipment leasing, consumer finance, commercial real estate finance, venture debt, and infrastructure lending[8][12]. Structured credit includes investments in securitized loans such as collateralized loan obligations (CLOs) and asset-backed securities (ABS)[11].

4. 2026 Market Size and Growth Projections — Quantified Forecasts

Current Market Size and Forward Projections

The private credit market entered 2026 with substantial momentum. According to Moody’s 2026 Outlook, private credit assets under management (AUM) are expected to exceed \$2 trillion in 2026[1], marking a significant expansion of the asset class. Looking at the medium-term trajectory, the market is anticipated to approach \$4 trillion by 2030[1].

An alternative projection from Percent and Morgan Stanley, based on a \$3 trillion baseline at the start of 2025, projects the market reaching approximately \$5 trillion by 2029[13][12]. This represents substantial continued expansion from current levels.

Key Insight: Industry forecasters focus on market size projections rather than explicit year-over-year percentage growth rates. The variance in baseline estimates (\$2 trillion vs. \$3 trillion) reflects different measurement methodologies—some include only direct lending, while others incorporate specialty finance, structured credit, and asset-backed finance.

Implied Growth Rates Through 2030

Based on available market size projections, the implied compound annual growth rate (CAGR) through 2030 ranges from 13.6% to 18.9%:

Percent/Morgan Stanley Pathway: – 2025: \$3,000B – 2026: \$3,409B (implied) – 2029: \$5,000B – Implied CAGR: 13.6% (2025-2029)

Moody’s Pathway: – 2026: \$2,000B – 2030: \$4,000B – Implied CAGR: 18.9% (2026-2030)

The trajectory from current levels to 2030 implies approximately doubling of AUM over a 4-year period[1], representing continued robust expansion despite market maturation.

Segment-Specific Growth Dynamics

Evergreen Fund Explosion: The evergreen fund segment is experiencing explosive growth, with year-over-year growth of 45% as of June 30, 2025[2]. At Goldman Sachs, the ‘semi-liquid’ NAV was reported at \$426-430 billion in Q3 2025, following a 40% compound annual growth rate (CAGR) since 2021[3].

Private Wealth Expansion: Private wealth vehicles are expanding aggressively. Within the private wealth segment, private credit currently dominates, accounting for approximately 50% of private wealth retail net asset value based on Goldman Sachs data as of September 2025[2][3]. Gross inflows across diversified private wealth products show strong momentum, with 60-70% annualized growth rate in Q3 2025[3].

Perpetual Capital Structures: The five largest listed private credit managers (Apollo, Ares, Blackstone, Carlyle, and KKR) currently manage a combined \$1.5 trillion in perpetual capital, representing around 40% of their combined AuM[2]. If the CAGR seen since 2021 continues, these firms are projected to manage almost \$5 trillion in permanent capital by the end of the decade[2].

Addressable Market Context

The addressable market for private credit extends beyond sponsor-backed lending into the real economy, exceeding \$30 trillion[1]. The current market size of \$2-3 trillion represents only 7-10% penetration of this addressable opportunity, suggesting substantial runway for continued expansion.

A major growth opportunity exists through the US defined-contribution market. Following an executive order signed in August 2025, the Department of Labor and SEC are detailing how illiquid assets including private credit could be incorporated into 401(k) plans, potentially unlocking an estimated \$12 trillion market[3].

5. Growth Drivers for 2026 — Structural and Cyclical Catalysts

Asset-Backed Finance Leading Growth

Asset-Backed Finance (ABF) is expected to lead growth in 2026, driven by alternative asset managers expanding into newer, more diverse asset pools including consumer loans and data infrastructure credit[1]. New partnerships with banks and financial institutions are spurring origination opportunities as banks remain constrained in certain lending activities[1].

Segment Fundraising Momentum (2025 Data Indicating 2026 Trends)

Direct Lending: Raised \$79 billion in 2025[2], maintaining its position as the largest strategy by AUM.

Specialty Finance Breakthrough: Achieved a breakthrough with \$37 billion in fundraising in 2025—more than the previous two years combined[2]. In the first three quarters of 2025, specialty finance accounted for 34% of all funds in development, up from 23% in 2024[2]. This shift represents a major evolution in the market’s composition, with specialty finance now competing with direct lending as a primary strategy.

NAV Lending: 2025 saw record \$12.9 billion of NAV lending fund closes, including 17Capital Strategic Lending Fund 6 at \$5.5 billion, the largest fund ever closed in the asset class[2].

Credit Secondaries: The first three quarters of 2025 saw record credit secondaries fundraising of \$16 billion—more than the previous three years combined[2]. Fund manager-led continuation vehicles have overtaken allocator-led deals for the first time, with over \$7 billion of credit continuation vehicles closed in 2025[2].

Deal Activity and Deployment Momentum

Fourth-quarter 2026 deal screening activity for private credit was up more than 25% year-over-year[1], indicating robust pipeline development. In 2024, global leveraged finance issuance reached approximately \$1.2 trillion, representing a 92% increase from 2023 and among the highest years on record[14]. U.S. leveraged loan issuance reached \$654 billion in 2024, doubling from the prior year and the highest total outside the 2021 pandemic-era boom[14].

Technology Infrastructure and AI Data Centers

AI infrastructure financing is expected to drive significant issuance across public and private debt markets, with hyperscaler CapEx expected to increase 45% year-over-year in 2026[4][5]. AI data center and power capacity demand creates substantial origination opportunities for private credit lenders with expertise in infrastructure and project finance.

6. Geographic Growth Patterns — Regional Dynamics

Europe: The Major Growth Hub

European private credit experienced a significant structural shift in 2025. European fundraising hit a record \$65 billion through the first nine months of 2025—14% higher than 2024’s full-year total of \$57 billion[2]. European funds accounted for 35% of all private debt fundraising in the first nine months of 2025, up from roughly 24% in 2023 and 2024[2].

Key drivers for European growth include: – Basel IV implementation expected to drive further migration from bank lending toward private debt[2] – Europe remains a more diffuse and inefficient market compared to the US, meaning there are still opportunities for wider spreads[2] – Infrastructure and defense spending plans creating substantial origination opportunities[2] – Two €10 billion+ mega-funds closed in 2025, including Ares Management’s record-breaking Ares Capital Europe VI at €17.1 billion[2]

Additionally, 60-80% of European sponsors’ M&A activity in 2025 was funded by private credit, favoring deals with shorter holding periods and rapid turnover[28].

North America: Temporary Softness

North America-specific funds raised just \$52 billion over the first nine months of 2025, or 28% of the overall total—a sharp fall from 2023 and 2024, when North America accounted for around half of all private credit fundraising[2]. However, analysts expect this decline to be temporary, driven by economic volatility in the US rather than fundamental weakening of the market.

Multi-Region and Asia

Multi-region funds raised \$70 billion, or 37% of the total, in the first nine months of 2025[2], reflecting the globalization of private credit strategies and cross-border capital flows.

Asia private credit fundraising remained largely stable in 2025, though it outperformed 2024 significantly, particularly in Q4[1]. Non-bank credit penetration in Asia lags Europe and the US by a significant margin, suggesting gradual growth potential[1].

7. Market Structure and Key Players — Concentration and Leadership

Top Private Credit Managers

The private credit sector is heavily concentrated, with top managers including Oaktree, Ares, Goldman Sachs, HPS Investment, and Blackstone[9]. The top 10 U.S. private debt fund managers hold approximately 40-45 percent of all dry powder in the U.S.[9].

Apollo Global Management is positioned as a leading player in private credit, managing \$616 billion in credit assets as of December 31, 2024, representing the largest credit strategy within its Asset Management segment of \$751 billion total AUM[15]. Apollo’s credit strategy encompasses direct origination, asset-backed securities, multi-credit strategies, and opportunistic credit products[15].

Carlyle Group’s Global Credit segment represents another major private credit player, with \$192.4 billion in total Global Credit AUM and \$154.2 billion in fee-earning AUM as of December 31, 2024[14]. The company deployed \$24.5 billion in 2024 across its credit platform, including \$3.7 billion in direct lending and ten new collateralized loan obligations[14].

2024 Performance and Revenue Metrics

Apollo’s credit strategy demonstrated strong performance and revenue generation in 2024: – Management fees: \$1.9 billion (up 7.2% from \$1.8 billion in 2023)[15] – Advisory and transaction fees: \$822 million (up 31.9% from \$623 million in 2023)[15] – Credit Strategies funds generated \$113 million in performance allocations during 2024[15]

Carlyle Group’s Global Credit segment captured over two-thirds of Carlyle’s total \$40.8 billion in capital inflows during 2024, exceeding the company’s previously announced \$40 billion fundraising target[14]. Carlyle’s Global Credit carry funds (approximately 11% of Global Credit’s remaining fair value) appreciated 12% in 2024, reflecting favorable market conditions[14].

Institutional Capital Sources

Private credit managers raise capital from institutional investors including pension funds, insurance companies, family offices, sovereign wealth funds, and high-net-worth individuals[9]. The continued growth of perpetual capital structures and evergreen funds reflects institutional recognition of private credit’s role in diversified portfolios.

8. Regulatory Landscape and Oversight — Evolving Framework

Current Regulatory Architecture

Private credit regulation in the United States is characterized by a fragmented approach, with oversight shared among multiple regulatory agencies rather than concentrated under a single regulator[16]:

Primary Regulatory Bodies: – SEC (Securities and Exchange Commission): Regulates investment advisers to private credit funds under the Investment Advisers Act; many private credit managers must file Form PF[16][17] – CFTC (Commodities Futures Trading Commission): Provides oversight when derivatives are involved or for funds registered as CPO/CTA; requires joint Form PF filings[16][17] – State Regulators: Handle adviser registration for smaller advisers and oversee nonbank lending and usury licensing[16] – Federal Banking Regulators (Federal Reserve, OCC, FDIC): Supervise banks’ exposures to private credit through revised reporting requirements[16] – FSOC/Federal Reserve/GAO: Monitor market-wide risks and assess potential systemic risk[16]

Recent Regulatory Developments (2023-2025)

Form PF Amendments (February 2024): The SEC and CFTC finalized amendments to Form PF—a filing required of SEC-registered investment advisers with at least \$150 million in private fund assets under management—to strengthen oversight of private credit funds and assist FSOC in monitoring systemic risks[17].

However, the regulatory posture has shifted in 2025 under the second Trump Administration and SEC Chairman Paul Atkins, with the SEC withdrawing several Gensler-era rule proposals that would have added significant compliance obligations for private credit fund managers regarding cybersecurity, vendor due diligence, and custody[19]. The SEC has also delayed compliance with new Form PF requirements and is expected to undertake a broader review of Form PF[19].

Enhanced Bank Reporting Requirements: Federal banking regulators on December 27, 2023, proposed new reporting requirements for bank loans to private credit lenders and intermediaries[23]. Banks are required to report loans to private credit intermediaries in distinct categories, reflecting the growth from \$56 billion in 2010 to \$786 billion in 2023—approximately 6.4% of total bank lending[23]. These requirements were finalized in 2024[17].

Federal Reserve Capital Reporting (June 2024): In June 2024, the Federal Reserve proposed requiring banks to report additional information in their capital and stress-testing reports (Form FR Y-14) on their lending to private credit funds and other nonbank financial institutions[17].

FSOC Oversight Assessment (October 2024): On October 18, 2024, the U.S. Financial Stability Oversight Council reviewed regulators’ efforts to increase monitoring of the private credit industry, noting that “the current lack of transparency in the private credit market can make it challenging for regulators to fully assess the buildup of risks in the sector”[17].

Systemic Risk Concerns and Congressional Scrutiny

Regulators and policymakers have identified several critical risk areas:

Synthetic Risk Transfers (SRTs): Banks increasingly use SRTs to transfer credit risk to private credit funds, allowing banks to reduce required capital holdings. As of October 2024, \$1 trillion in loans globally are now tied to SRTs[20]. These complex arrangements create layers of interconnected leverage that are not fully visible to regulators[20].

Leverage and Valuation Concerns: Companies borrowing in private credit markets tend to be smaller and carry more debt than companies with traditional capital structures[20]. Private loan valuations are more opaque and often more generous than valuations set by public markets[20]. Firms may assign different values to the same credit investment based on their own policies, internal models, and subjective evaluation of available data[21][22].

In November 2023, U.S. Senators Sherrod Brown (D-OH) and Jack Reed (D-RI) urged federal banking regulators to assess the potential risks posed by the growing private credit market[18]. The Senators expressed concern that “private credit funds operate in the shadows” with “minimal, indirect regulatory oversight” and insufficient insight into loan terms, funding structures, and borrowers’ financial health[18]. On December 20, 2024, the same Senators reaffirmed their concerns, emphasizing that risks have intensified as the market has grown in size and complexity[20].

Stability Assessment and Industry Response

A May 2023 Federal Reserve Financial Stability Report found that private funds’ lending activities had not threatened financial stability—findings mirrored in a 2020 Government Accountability Office report[16]. Private credit default rates remain limited due to strong debt structure, contractual provisions minimizing defaults, and underwriting that protects lenders and investors[16].

The Managed Funds Association contends that private credit markets are not as opaque as regulators claim, arguing that substantial data is available to policymakers and the public through multiple channels including Form PF filings, bank call reports, BDC quarterly disclosures, insurance company state filings, and UCC financing statements[17].

9. Private Credit Within the Alternative Investment Ecosystem

Positioning Relative to Private Equity

Private credit and private equity represent fundamentally different investment approaches within alternatives. The key distinctions are:

| Dimension | Private Credit | Private Equity |

|---|---|---|

| Investment Type | Debt financing (loans) | Equity ownership |

| Return Source | Interest payments + fees | Capital appreciation |

| Historical Returns | ~10.1% average (15 years) | 15-25%+ net IRR |

| Risk Profile | Lower (senior secured) | Higher (equity exposure) |

| Holding Period | 3-7 years (defined maturity) | 5-10+ years (median 5.6) |

| Control & Involvement | Passive (monitoring only) | Active (board seats, operations) |

| Tax Treatment | Ordinary income rates | Long-term capital gains |

| Fee Structure | ~1.5% mgmt + 15% carry | 2% mgmt + 20% carry |

| Liquidity | Some quarterly options | Long lock-ups |

Private credit involves debt financing where investors provide loans to companies but do not acquire ownership stakes[24][25]. Returns are generated through interest payments and fees on loans, providing predictable, steady income, with historical returns for private credit averaging around 10.1% over the last fifteen years[26]. In contrast, private equity entails equity investment where investors acquire ownership stakes in private companies with the goal of increasing company value through operational improvements and strategic initiatives[24]. Private equity returns depend on capital appreciation through company growth and successful exit strategies, and are back-loaded, with returns primarily realized when the company is sold or goes public[27][29].

2026 Return Profiles Across Alternative Investments

According to 2026 market data, private credit funds deliver 8–12% yield with moderate risk and a 2–5 year lockup period, positioned for income-focused investors[30]. This compares to other major alternative asset classes as follows:

| Asset Class | Return Profile | Risk Level | Liquidity |

|---|---|---|---|

| Private Credit | 8-12% yield | Moderate | 2-5 year lockup |

| Multifamily Real Estate | 12-18% IRR, 6-9% cash flow | Moderate | 2-10 year hold |

| Ground-Up Development | 18-25%+ IRR | High | 3-7 year lockup |

| Private Equity Funds | 15-25%+ net IRR | Moderate-High | 7-10 year lockup |

| Hedge Funds | 8-15% returns | Moderate-High | Quarterly-annual |

| Venture Capital | 20%+ potential | High | 8-12 year lockup |

| Public REITs | 8-12% returns | Moderate | Daily liquidity |

Private credit stands apart from equity-focused alternatives because returns are primarily income-driven rather than appreciation-driven, delivering steady yield and lower volatility even when equity markets are volatile[30].

Portfolio Diversification Benefits

Private credit exhibits low correlation with traditional asset classes like stocks and bonds, providing portfolio diversification benefits[31]. The income-driven nature of private credit contributes to its diversification properties—unlike equity investments that move with public market cycles, private credit returns are driven by contractual interest payments and fees rather than equity market sentiment[30].

Over the past 10 years, private credit has delivered higher returns and lower volatility compared to both leveraged loans and high-yield bonds[12]. During seven periods of rising rates since 2008, direct lending averaged 11.6% returns, compared to its long-term average[12]. Private credit continues to offer significant outperformance relative to public alternatives, with excess returns of 200-250 basis points over leveraged loans historically[1].

Income Stability and Complementary Risk Profile: Private credit delivers steady yield from contractual loan payments, offering more predictable returns than growth-oriented alternatives[30]. Its moderate risk profile, supported by secured collateral and priority claims in default scenarios, distinguishes it from both high-risk equity investments (private equity, venture capital) and lower-return traditional debt (public bonds)[30].

10. Market Dynamics and Late-Cycle Considerations

Transition to Quality and Selectivity

The private credit market is transitioning from yield-driven momentum to underwriting-driven returns[13]. Late-cycle conditions favor strategies with strong collateral, cash-flow visibility, amortization, and conservative structures[3]. Performance dispersion within private credit is widening in 2026, with larger businesses continuing to outperform while smaller companies face challenges, underscoring the importance of manager quality and strategy selection over market momentum[1].

According to Percent’s 2026 Private Credit Outlook, “the next wave of growth will be defined by discipline, not hype”[13]. The market is entering a more demanding phase where capital flows toward managers with strong structuring, transparent data, frequent reporting, and tight risk/operational oversight[13].

Credit Quality Concerns

While headline default rates have remained below 2% for several years, when selective defaults and liability management exercises are included, the “true” default rate approaches 5%[2]. The International Monetary Fund’s 2025 Financial Stability Report found that around 40% of private credit borrowers have negative free cash flow—up from 25% in 2021[2].

Payment-in-Kind (PIK) usage has risen notably, with public BDCs now receiving an average of 8% of investment income via PIK, suggesting borrowers are struggling under higher interest burdens[2]. Additionally, private credit raises overall corporate leverage, potentially making the corporate sector more vulnerable to financial shocks[9]. Interest coverage ratios have declined significantly, with mean interest coverage at around 2.0x—below the 2.7x for leveraged loan borrowers[9].

Despite increasing first-lien securitization, private credit loans have relatively low recovery rates upon default compared to syndicated loans, with post-default values around 33 percent versus 52 percent for syndicated loans[9].

Key Investment Considerations

Illiquidity Risk: Private credit is illiquid by nature—investors may need to lock capital for 5-10 years and face steep losses if requiring emergency exits[8]. While some private credit vehicles offer quarterly liquidity options[29], the underlying loans are often illiquid and bespoke, creating potential liquidity mismatch risk where redemption pressures in downturns could lead to fire sales[19][20].

Fee Structures: Private credit funds charge significant acquisition fees, annual management fees, and other charges well exceeding those of index funds[8]. However, median management fees around 1.5% and carried interest around 15%[24][26] are generally lower than traditional private equity’s “2 and 20” model.

Investor Suitability: Private credit typically requires minimum investments of \$100K-\$250K, making it more accessible than private equity or venture capital[30]. This positioning makes private credit attractive to high-net-worth individuals, family offices, and institutional investors with accreditation status seeking reliable income with lower volatility[30].

Conclusion

Private credit has evolved from a niche financing source into a \$2-3 trillion mainstream alternative asset class that is fundamentally reshaping corporate finance. The asset class is projected to achieve robust growth through 2026 and beyond, with market size expected to exceed \$2 trillion in 2026 and approach \$4-5 trillion by 2029-2030, representing a 13.6-18.9% compound annual growth rate.

This expansion is driven by structural forces including bank lending retrenchment (particularly Basel IV in Europe), institutional capital allocation toward alternatives, perpetual capital innovations (evergreen funds growing at 45% annually), and an addressable market exceeding \$30 trillion. Geographic diversification is accelerating, with Europe leading fundraising at \$65 billion in 2025, while specialty finance and asset-backed finance are emerging as high-growth segments challenging direct lending’s dominance.

However, the market is maturing into a more selective phase. The transition from yield-driven momentum to discipline-focused underwriting reflects rising credit quality concerns—40% of borrowers have negative free cash flow, and true default rates approach 5% when including liability management exercises. Regulatory oversight is intensifying through enhanced Form PF requirements and bank reporting obligations, though systemic risk assessments suggest the market does not currently threaten financial stability.

For investors, private credit offers compelling diversification benefits through low correlation with traditional assets, steady income generation (8-12% yields), and moderate risk profiles supported by senior-secured positions. The asset class occupies a distinct niche within alternatives—providing income-focused returns complementary to equity-oriented strategies like private equity and venture capital. As the market enters 2026, success will increasingly depend on manager quality, underwriting discipline, and transparency—rewarding lenders who prioritize downside protection over aggressive yield chasing in an expanding but increasingly competitive landscape.

Sources

[1] Private credit outlook 2026 executive summary

[2] Private Credit Outlook 2026: The Market Faces its First Big Test

[3] Private Markets Outlook 2026 | UBP

[4] 2026 Credit Outlook: From Scarcity to Selection—The Return of a Buyer’s Market – Apollo Academy

[5] 2026 Investment Perspectives – Blackstone

[6] Private Credit: An Introduction

[7] Private Credit Investing: What You Need to Know | KKR

[8] Private Credit Investing: Strategies & How It Works

[9] The Fed – Private Credit: Characteristics and Risks

[10] Essentials of Private Credit Investing – Blackstone

[11] What is private credit? And why investors are paying attention

[12] Private Credit Outlook: Estimated $5 Trillion Market by 2029 | Morgan Stanley

[13] Percent Releases 2026 Private Credit Outlook: Growth Continues as Scrutiny Intensifies

[14] Carlyle Group Inc. (CG) 10-K – 2025-02-27 Part 2 – Item 7

[15] Apollo Global Management, Inc. (APO) 10-K – 2025-02-24 Part 2 – Item 7

[16] Private Credit – Managed Funds Association

[17] Regulatory Coverage: US Regulators Consider Increased Monitoring of Private Credit Industry – Octus

[18] Brown, Reed Warn Regulators of Risks Posed by Private Credit Market | United States Committee on Banking, Housing, and Urban Affairs

[19] Private Credit | Growth, Access & Policy Shifts

[20] Brown, Reed Raise Concerns on the Growing Risks of the Private Credit Market | United States Committee on Banking, Housing, and Urban Affairs

[21] Three Risks to Monitor in Private Credit | The Capital Commitment

[22] Three Risks to Monitor in Private Credit – Insights – Proskauer Rose LLP

[23] Private Credit Reporting Requirements Proposed by US Banking Regulators | Insights | Mayer Brown

[24] Private Credit vs. Private Equity: Differences and Skills for Success

[25] Private Credit vs. Private Equity | Allvue Systems

[26] Private Equity vs Private Credit: Key Differences Explained

[27] Private Credit vs. Private Equity: Pros and Cons for Investors

[28] Private Credit vs Private Equity: Differences, Risks & Benefits Explained

[29] Comparing Private Equity & Private Credit for High-Net-Worth Investors

[30] Top Alternative Investments for Accredited Investors in 2026

[31] Alternative Investments 101: A Beginner’s Guide | SoFi